-

Wherever you invest for the long term the government will find a way to take at least some of it from you if they need it.

There's no guarantee you'll be around to take advantage of the long term investment either.

So edge your bets by spreading long term investments across several classes and do the same with your money overall, investing in your life and that of your family's now. Whether that be a nice home, vehicles, hobbies, adventures, ...

Some of the best things for your mental and general health are relatively cheap to access so don't cost a lot of investment either.

Plan for the future but don't forget to enjoy the now.

Leave a comment:

-

Well off? That made me laugh. How well off do you imagine I am?Originally posted by b0redom View Post

I'm not advocating all crypto will be around in years to come. What I am saying is we're in the grip of a fully fledged bull market that's going to rocket even further in 2018. I'm advocating you benefit from that and get out before the bubble comes.

Stake only what you can afford to loose. You're probably loosing more just holding it in the bank account against inflation with each passing day. Get smart, not Drei grumpy.

I've told you, Zencash, will explode in the coming 12 months. A good 6-12 months before the bubble bursts.Leave a comment:

-

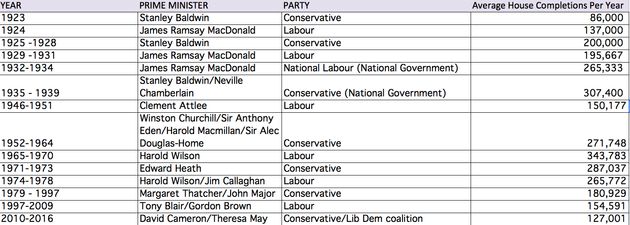

Every country has seen population growth, Germany 1m+ and is coping.Originally posted by d000hg View Post

Truth be told UK government is building far less houses than ever before. If companies were scrambling over themselves these statistics would look a lot different.

Leave a comment:

-

Property versus pension?

Why not property AND pension or property AND ISA? Even better, no risk of rental voids or idiot tenants wrecking the place.

Here is a (fairly) undiscovered gem for you to pop into your SIPP or ISA, then forget about it and let the income roll up tax free for the next 30 years. Sounds good? Take a look at buying a stake in a >GBP 300 million property portfolio. Look specifically at Regional REIT. Pays >8% a year dividend, tax free in an ISA or SIPP. Even better, the shares are available at a small discount to net asset value. Pop a nice slice of Regional REIT in your pension, then thank me in 30 years time

Leave a comment:

-

I've seen your posts in the crypto thread. It would be great to buy a bunch of crypto currency and pay off my mortgage in a couple of weeks. Problem is that is exactly what everyone said in the early 2000s. It's free money, how can this website possibly fail etc....Originally posted by scooterscot View Post

Despite what you think there's no guarantee crypto currencies will be around in a year, month, week even a day. They're not backed by anything (which I get is part of the attraction). Don't get me wrong, I've got a chunk of change sitting depreciating in a bank account and I'd love to get a 100%+ return on my investment, but as much as I'd like that, I'd hate to lose it more.

Honestly, if you're as well off as you're making out, I don't understand why you don't cash out and live the billionaire lifestyle, rather than posting on here and visiting rubbish hotels when you come to the UK.Leave a comment:

-

Population growth remains as does housing pressure... companies are scrambling over themselves to build more houses fast enough. We've been talking about a correction in house prices at least 10 years and even factoring in the peak of ~2005 it hasn't really happened.Originally posted by scooterscot View Post

I'm trying to recall if the IFA running the sums with me for ISA VS pension was factoring in higher rate tax or not. IIRC you're paying CT regardless so the difference is in the ISA you pay the 'top up' to HR tax, but the pension you pay tax on your income later.Originally posted by TheCyclingProgrammer View Post

He definitely suggested it wasn't a huge difference but again I cannot recall the exact earnings scenario it was based on.Leave a comment:

-

Crypto has always been an abbreviation of cryptography to me, not crypto currency.Originally posted by Lance View PostLeave a comment:

-

Agree. BTL is dead.

Not specifically because of Brexit or government policy. But more the realisation the housing market is overinflated and a correction is likely. As such potential yield is now at a minimum. Plus there's the risk your BTL mortgage might be worth more than the asset in the coming years. Sod that.

There's far less risker investments out there. I'm not going to say it.Leave a comment:

-

Good evening! So I'm basically the same boat as you - 31 and no pension worth mentioning. We do own our own home (with a mortgage, not outright) and we were able to get a great deposit down it. It's something I worry about a LOT, though I know I'm far from alone in this boat and at least I've managed to do some great life things til now so there's that.

Right now I've basically come to the conclusion that property will be my first call. I'm juuuuuust coming to the point where I can seriously start considering getting a deposit down on something modest (£25k ish on a £100kish property) to let out.

My plan is to get a 25 year mortgage and aim to break even on the property over that time. The theory being that in 25 years time I then have a fully paid for asset, which I can then do as I please with. I've not looked at proper proper figures, but it should be pretty much doable.

Contentious opinion alert: I agree that the major boom years of BTL are probably over, but I don't care what anyone says. We're on a small island - at best our population will stagnate to a degree, but in essence property and land is always going to be a valuable commodity. Absolute worst case, I think I'll end up owning a property that's simply gone up with inflation - i.e., have the equivalent of £100k in todays money. Personally, I suspect things will work out far better than that over the years.

That said, once I've done that, my plan is very much to start piling something into a pension. I can't bring myself to chuck in crazy amounts, but diversification is definitely important.

Beyond that, like you, I figure I can do it once I can maybe do it again.Leave a comment:

Leave a comment: