Originally posted by vetran

View Post

-

went in to change a detail on a bank account. Apparently I'm pre approved to borrow 10s of thousands as a personal loan... would you like them to call you sir?Originally posted by Ticktock View Post

they haven't learnt.

Whilst I'll be miffed as I got a repayment mortgage I doubted endowment mortgage would work (friends found they didn't) I suspect they will win and the Banks will pay out.Leave a comment:

-

indeed...oh and a belated Happy BirthdayOriginally posted by BrilloPad View Post

Leave a comment:

-

Let them sue, if they win it would be big enough to destroy the banks.Originally posted by DimPrawn View Post

But I don't think they will win;-)Leave a comment:

-

I know a few people doing this. They have and have always had an interest only mortgage. They also have absolutely no way of paying off the capital. They have spend the money that should have gone onto paying the capital on fancy cars and lots of holidays.Originally posted by Ticktock View Post

When I discussed how they will cope when the bank asks for the capital, they said "There's millions like me, we will sue the banks for misselling and get the house for free".

And the sad thing is, they probably will, and they will win.Leave a comment:

-

-

Good spot with the IR hike - carts an horses but might have had an effect on things.Originally posted by BlasterBates View Post

No we won't have a Japanese style crash, we will have a UK one ;-)

Leave a comment:

-

Don't get me wrong, I'm not saying there won't be a crash.

There will be.

But not yet.

and by the way did you spot the interest hike just before the Japanese bubble popped.

Stock market valuations were way way higher in Japan than they are now in the FTSE, 4 times as high. The average PE ratio on the Japanese stock market in 1990 was 60. This was comparable with tech stocks in 2001.

The average PE ratio in the FTSE is about 15. There is not going to be a Japanese style crash.Last edited by BlasterBates; 4 September 2015, 12:19.Leave a comment:

-

And now we get the news that lots of people who took interest only mortgages can't afford to repay them.

Of course, the news is how nasty the banks were letting them have the money when they obviously couldn't afford it. Not how stupid these people were to take a loan they couldn't repay. Much wringing of hands over how to help these people keep "their" homes.

The simple answer is that if they hadn't borrowed money they couldn't afford, in the same way as people who borrowed more income multiples than they should, or took 125% of house value on a 100% loan as they couldn't afford a deposit, then house price inflation wouldn't have been supported to the levels it has been.

But remember - if you borrow money you can't afford, it's never your fault, it's always the bankers who forced the cash into your hands.Leave a comment:

-

The fundamentals are that house prices outside London are not excessive.Originally posted by PurpleGorilla View Post

Both the stock market and houses are not yet due for a crash, first of all interest rates need to be jacked up. Then there will be a crash.

Interest rates are part of the economic fundamentals that determine whether assets are under valued or over valued.Leave a comment:

-

Nope that's never going to happen, it's like you say DP high rates, low prices or low rates, high prices.Leave a comment:

-

Indeed. You can either have lower purchase price with very high monthly mortgage payments, or very high purchase price with lower monthly mortgage payments.Originally posted by BlasterBates View Post

What Mauve Monkey thinks we will get is low purchase prices with low monthly payments. That never happens I'm afraid.Leave a comment:

-

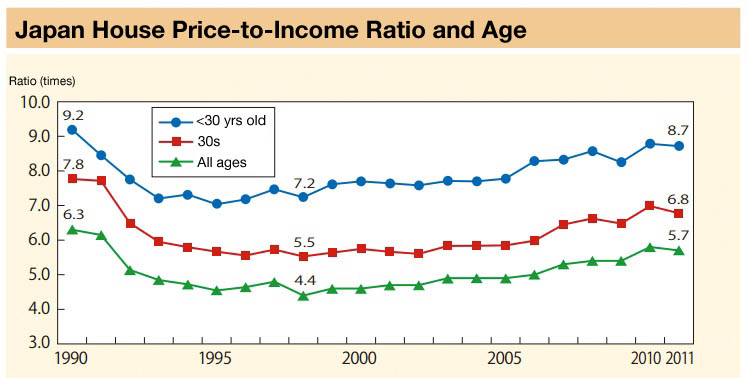

Not in Japan:Originally posted by BlasterBates View Post

I agree low IR has helped the bubble.

We are in unprecedented times regarding IR.

IR are now an irrelevance, the bubble will pop purely on fundamentals.Leave a comment:

-

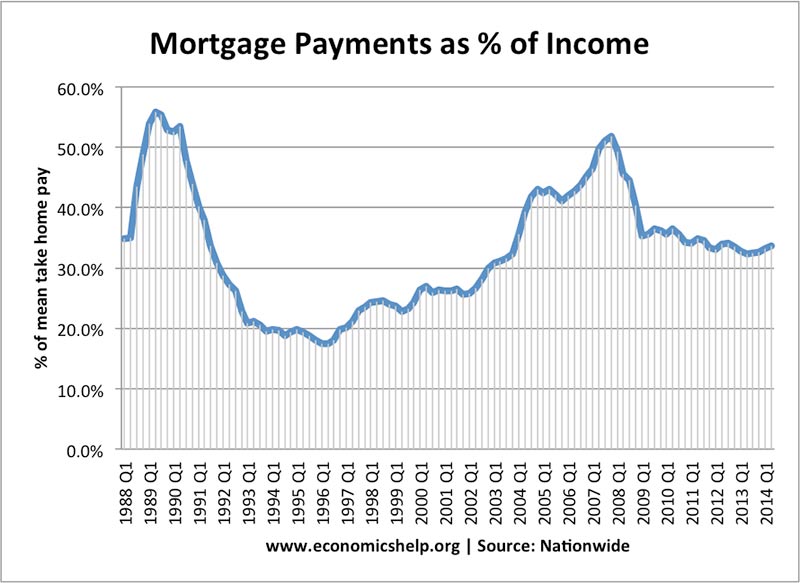

House prices are governed by interest rates:

Houses are currently not overpriced for the current interest rates. You can easily spot the where crashes occured in the above graph.

The next crash will occur in a few years when interest rates get jacked up.Leave a comment:

Leave a comment: