Originally posted by BlasterBates

View Post

-

Not at all.Originally posted by vetran View Post

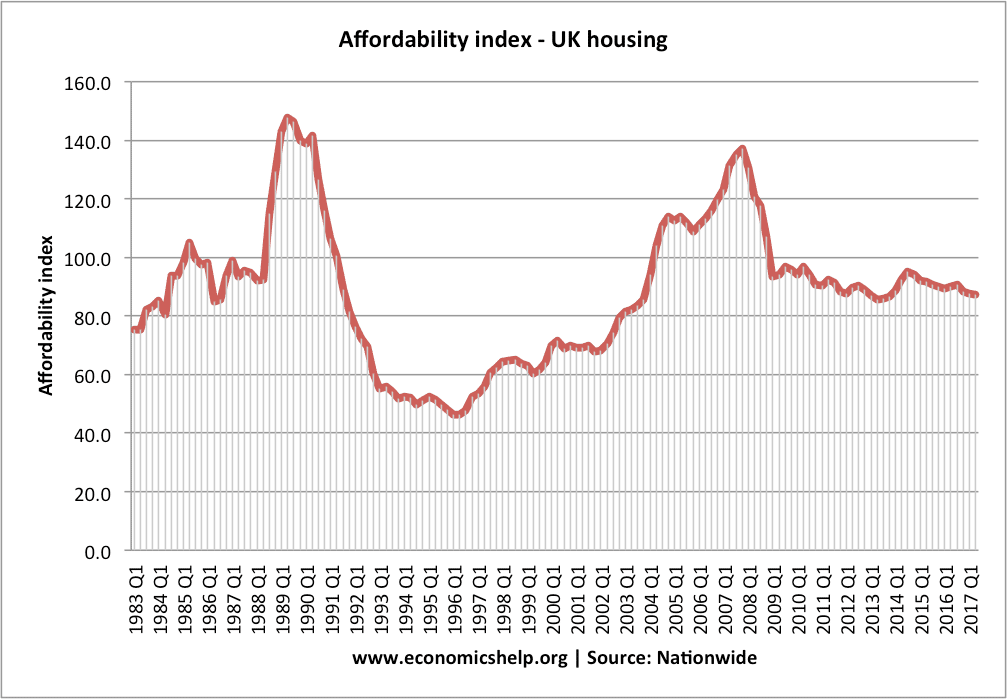

Mortgage payments are currently at 32% of mean take home pay. In 1980's it was consistently higher, in 1989 when interest rates shot up to around 15% it was 55%.Leave a comment:

-

I would remove or reduce student loans for those that study STEM subjects.

I would allow employers tax breaks for non-vocational training and apprenticeships.

But most importantly I will allow euthanisation of all the loud mouthed, inconsiderate twats that inhabit these isles, thus reducing population by at least 50%.Leave a comment:

-

Originally posted by BlasterBates View Post

Whilst comparing it to inflation may seem to make sense actually you should compare against wages when considering affordability.

Housing affordability in England and Wales - Office for National Statistics

Few people have been getting wage rises over the last few years.Leave a comment:

-

House prices are lower than they were 15 years agoOriginally posted by vetran View Post

House prices will drop when the interest rates go up, always have and they always will. You bought at a time that was very unusual just after a housing crash and the interest rates had just dropped. House prices shot up over a 10 year period, and over the following 15 years dropped in real terms.Leave a comment:

-

Originally posted by BlasterBates View Post

FTFY

If you are trying to say that because interest rates are low people are risking more debt than is sensible then unfortunately you are right. Its a balloon of debt and will end in trouble however the fact there is a shortage of stock may cushion it.Leave a comment:

-

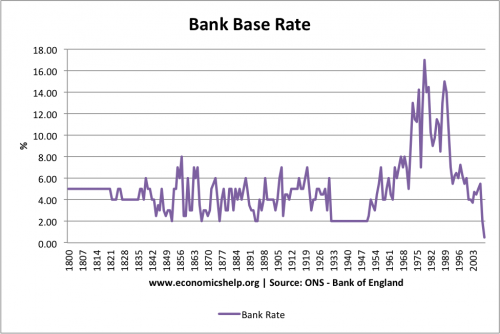

We're getting there. Here are the interest rates in the 1970's and 1980's.Originally posted by vetran View Post

Leave a comment:

-

Originally posted by BlasterBates View Post

so you don't repay the capital at all? The amount of interest you pay has no relation to the capital?

From your calculator

you borrow £200,000 at 1.6% (the default) you pay back £242,000

you borrow £100,000 at 3.2% you pay back £145,000Your monthly payment

£809.30

so doubling the price means you pay nearly 100k more even though the interest stays the same. Yes you pay 100% more interest if you double the interest rate but that is obvious.Your monthly payment

£484.68

However as to your point about affordability the doubled capital nearly doubles the repayments. Both mortgage examples have about 45k iinterestLeave a comment:

-

Most of what you pay for a house when you buy is interest.Originally posted by vetran View Post

Mortgage calculator

Double the interest rate and see what happens to your mortgage.Leave a comment:

Leave a comment: