Originally posted by Nixon Williams

View Post

-

With all the discussion through this thread, your calculator would become really valuable if it let you enter charitable giving as well and took that into account. -

Dividends are paid with a 10% tax credit - so a £900 dividend has a £100 tax credit making a total gross dividend of £1000.Originally posted by psychocandy View Post

To answer your point, effectively you could take £500 in a gross dividend, which would be £450 net, ie the actual amount declared and paid from the company account.

Our website has a dividend calculator that will allow you to put in your salary, dividends taken so far etc, and advise how much you can take before hitting the higher rate tax bracket, this is also available as an app, but I am not allowed to put a link on here.

Leave a comment:

-

Ah yes. But it doesnt save you any more tax if you're below the 40%....Originally posted by d000hg View PostLeave a comment:

-

It raises by £500 how much you can take as dividends before they attract higher tax.Leave a comment:

-

??? But CT is paid by the company and then tax credit applied to personal tax, isn't it?Originally posted by Nixon Williams View Post

If you're say £500 short of using up your full allowance via salary you don't then get to pay no tax on the first £500 of any dividends do you? (because its already been taxed via company as CT).Leave a comment:

-

You only 'lose' the tax allowance on the salary, however, assuming that you have other forms of income, probably dividends, then the unused tax allowance is taken account of here.Originally posted by psychocandy View Post

This assumes that your gross income does not exceed £100,000 as the tax allowance is gradually withdrawn above this level.

AlanLeave a comment:

-

FTFY.Originally posted by Master View Post

You need to file Nil returns instead though, to let HMRC know you haven't simply forgotten to pay, so overall admin about the same.

It would actually save a few pence* to pay right up to the Primary Threshold (£7748, 2013/14) even though this incurs NI, but the risk is you mess up or forget to pay and HMRC land you with a penalty.

* about a fiver a year, so only worth it on point of principle.Leave a comment:

-

Think I get it. OK so by not paying £8105 I'm basically losing £617 worth of tax free allowance yet? (So I'm paying 20% in effect by taking it as divi instead = £122.Originally posted by Nixon Williams View Post

But the reason for doing this is because if I did take it the employers and employee NI on this extra £617 would be more than the amount saved in tax? correct?Leave a comment:

-

TLDR - sorry

Absolutely - I took a tribunal case once on a pubs tax affairs, and we needed to evidence wastage when pipes were cleaned. Oh my old friend PI, how I missed thee for 20 yearsOriginally posted by d000hg View Post

Leave a comment:

-

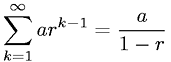

I was looking at this again, and was struck that if you give a fixed % of your profits to charity, you end up having to perform a geometric series summation to figure out to the penny what you can actually take.

e.g say your divi pre-tax limit is 30k and you set to give 10% to charity...

You take a £30,000 divi and give £3000 away. That is £3750 gross.

You take a £3750 divi and give £375 away. That is £468.75 gross.

You take a £468.75 divi and give £46.88 away. That is £58.60 gross.

...

So we are performing with a = £30,000 and r = 0.125:

with a = £30,000 and r = 0.125:

We end up with total divi = £30000 / 0.875 = £34285.71, charitable giving = £3428.57.

Who knew real maths could be useful in accounting!Last edited by d000hg; 20 February 2013, 12:52.Leave a comment:

-

Sadly, it is more complicated than it used to be.Originally posted by Pondlife View Post

For 2012/13:

Income tax is payable on income over £8,105

Employee's NIC is payable on income over £7,605

Employer's NIC is payable on income over £7,488

For 2013/14 the figures are:

Income tax is payable on income over £9,440

Employee's NIC is payable on income over £7,748

Employer's NIC is payable on income over £7,696Leave a comment:

-

Not quite right. I think the threshold is a bit lower than £7488 but, as you say, NI is due on anything above £7488 which is why its better to not use all of your tax free allowance.Originally posted by Pondlife View PostLeave a comment:

-

The 2013/14 salary that can be paid without any deductions for PAYE (assuming a standard code) and NIC, or any employer NIC will be £7,696 which amounts to £641 per month.Originally posted by Pondlife View Post

The tax free threshold will rise to £9,440 - the starting point for tax and NIC used to be the same but the Government's aim to raising the tax threshold appears to ignore the NIC that is payable on lower starting salaries.Leave a comment:

Leave a comment: