Originally posted by Hobosapien

View Post

-

I agree. And of course you did not mention Greece and the other Southern Euro countries.Originally posted by Hobosapien View Post

Initially people will feel like wage slaves. Then enough people will borrow with no intention of repaying. It will take in generation. In the meantime, party on Wayne. Paryy on Garth.Leave a comment:

-

Originally posted by BrilloPad View Post

Not necessarily. When no one is interested in paying back the debt only servicing the interest then as long as interest rates stay manageable the 'solution' can roll on for ages. They'll just try to deflate the debt by reducing the value of the currency it is held in.

See the USA and how they keep rolling on their national debt obligations. UK are just doing the same. No intention of paying back the debt, just need to avoid drowning under the interest charges. Same applies to consumers on easy mortgage rates and leasing for other things like cars.

So may as well spend spend spend. Worse that can happen is you have to declare bankrupt and they take the shiny stuff away, but unless things have changed very recently there is no desire to repossess houses due to bad mortgage payments, all part of the 'solution'. After a few years of being bankrupt can start again from a slightly worse off position credit wise.

Leave a comment:

-

Can you define imminent? I reckon imminent = another generation.

The normal economic cycle was ruined in the early noughties. The debt bubble "popped" in 2008. It was then decided that the solution was more debt.

Now the bubble is unburstable. It has to be kept inflating.

What I *want* to happen is for it to be burst asap as the longer it goes on the worse it gets. What will happen is that people will keep borrowing more and more and become wage slaves.Leave a comment:

-

Were you and the mods included in the sale of livestock?Originally posted by administrator View PostLeave a comment:

-

Not hit double figures since '91 but was common in the 70s and 80s by the looks of it. Could be interestingOriginally posted by shaunbhoy View Post

Leave a comment:

-

7.5% - is that all? My Mum enjoys telling me what is was like when interest rates were 15% or whatever it was when she and my dad bought the farm in the 80s. What are the chances that we will see rates like that again at some point?Leave a comment:

-

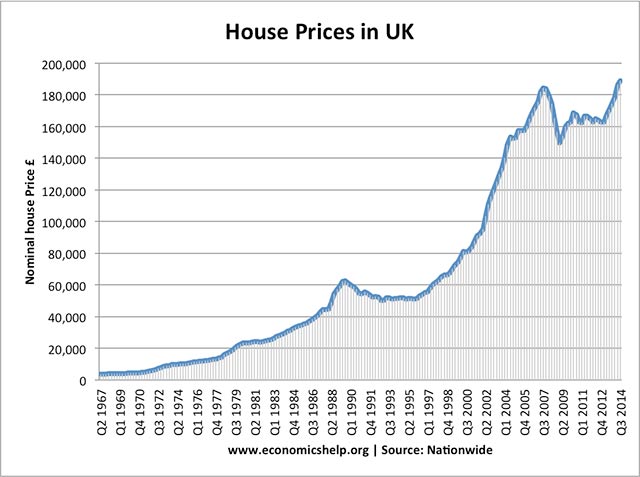

Graph doesn't look like much without earnings but the I'm quite certain the increase of earnings is not matching this slope. It'll normalise by about 40% me reckons. Be at least 1000 miles away what that bubble bursts.

Leave a comment:

-

Tory Brexit DOOM™: House Prices Crash now imminent

"Analysis by London & Country, the mortgage broker, found that someone who made monthly payments of £766 on a 25-year £200,000 mortgage could have to prove that they could afford repayments of £1,478 at a rate of 7.5pc."

Bank of England tightens mortgage rules: what it means for you

Leave a comment: