Originally posted by rambaugh

View Post

-

Quite correct about FX charges. Myself, the approach I take is the simplest. Just not buying anything unless it's priced in GBP. Given the thousands of options I have within that, I really don't have a problem. Mustn't lose sight of the fact we are considering low cost retail investment platforms here. Options are available for those wanting much more in the way of international markets exposure. For the majority of us, I suspect one of the usual suspect low cost retail platforms is all we really need.

-

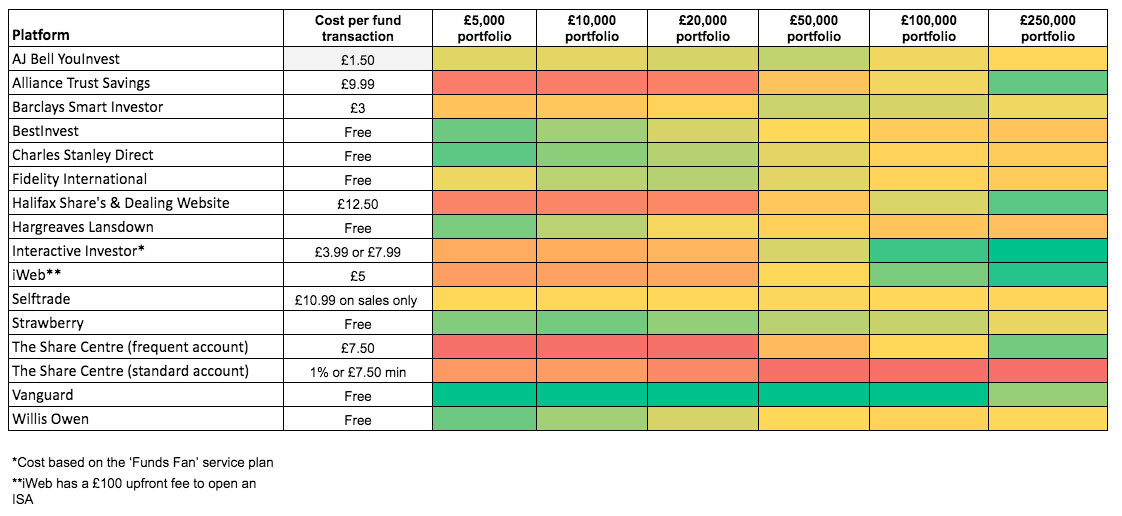

No one has yet mentioned the FX charges applied by II or HL when it comes to investing in anything other than investments based in GBP and was wondering if anyone had done the sums with II or HL in this scenario?

HL and II charge FX commission rates on investments made on their platforms which are not based in GBP. For example if you're interested in buying an ETF that has a base currency in USD you'll get slugged with a transaction charge when buying / selling. II's FX charges look quite hefty and start at 1.5% commission. HL's are not as bad at 0.25% for a similar investment amount. You could ofcourse only buy funds with a base currency in GBP but this would limit your investment universe.

Vanguard does not appear to apply FX charges and while it's account fee is percentage based (and then capped at £375) it may actually work out better than II in the long run if you're investing globally. One drawback with Vanguard is that you can only invest in Vanguard's funds.

Leave a comment:

-

It's when you try to move away from them that you finally work out what a horrible, cynical company they really are. Stick with it and just think of the money you save every single month. In my case it's in the thousands per year now.Originally posted by jmo21 View PostLeave a comment:

-

May not be relevant if your son invests monthly but be mindful of inactivity fees, if you don't trade per month or quarter.Originally posted by northernladuk View Post

Leave a comment:

-

If you are transferring away from HL you will experience epic foot dragging. They do absolutely everything they can to slow down the transfer process because they are losing your fees anyway and you can be sure they will charge you 0.45% right up to and including the day your transfer happens.Originally posted by jmo21 View PostLeave a comment:

-

Only just done this in the last week, so only just starting to get to grips with it. I said "just moved", but my in-speccie transfer will take up to 12 weeks apparently. The interface is not as "shiny" as HL, but it'll probably be fine once I get used to it.Originally posted by northernladuk View Post

Plenty of my existing funds are available, but there are a few, where the class I hold is not available to purchase at the moment (remains to be seen if this is temporary). They have other classes available, so I have asked the question as to what will happen with my in-speccie transfer of those funds.

They are super slow to answer messages at the moment (5 day lead time, to be fair they do warn you) which has frustrated me enormously this week. I ended up phoning them to get something sorted, as when they finally responded to a message, they didn't take time to look at previous message on the subject.

So not the greatest start tbh, but prepared to give them the benefit of the doubt, as the savings will be enormous compared to HL.

I've been meaning to move for a couple of years, but never got round to it.Last edited by jmo21; 13 February 2021, 12:44.Leave a comment:

-

I use Vanguard and find it easy to use with a good mix of funds available to choose from within the ISA wrapper. Mrs W used this too, as did the other wealth managers in her Co. for their ISAs so I took that as a good enough recommendation personally.Originally posted by northernladuk View PostLeave a comment:

-

Good luck with your plans.Originally posted by rootsnall View PostLeave a comment:

-

I've just been active due to the whacko year we have had, I am trying to go buy and hold at some stage but the next crash comes just when you get too relaxed. The different outfits are in various stages of trying to attract custom and trying to then milk that custom. HL seem to be hoping that enough people will just stick to them and fill their coffers. My next move will be to get the cheapest when I'm in drawdown.Originally posted by Fred Bloggs View PostLeave a comment:

-

Indeed, but due diligence is required here. II have three service plan levels depending on how active you are, you need to check which is best for you. HTH.Originally posted by rootsnall View PostLeave a comment:

-

I switched to IWeb to hold the 0.05-0.07% cost funds but have ditched funds completely now due to the delayed sale aspect, even if it is priced the same day it's an uncomfortable wait compared to selling an ETF. I can't see any reason to use funds any more as you can cover everything with ITs and ETFs !? If you trade a lot then I don't think you'll beat IWeb. For research I used to use an old empty HL account but have gradually stopped using it. Mmmmm, II have got cheaper now, so maybe are the cheapest.Originally posted by sludgesurfer View PostLast edited by rootsnall; 12 February 2021, 10:19.Leave a comment:

-

Not as slick as HL, but then, nowhere is. (Though HL's slick website does rather alarmingly sometimes have incorrect or out of date information about dividends etc... More than you'd think without really looking). II is a whole of market retail platform, not restricted in any way. And the website is still improving since they are continuing to expand by acquisition. They are now #2 retail platform behind HL in the UK. All the information and more, is there at the II website and their customer service has got a lot better the last year or two. What I often point out is that as a non account holder at HL you can do everything you always did except to trade with them. I often use their website for a glance at stocks - Google for "HL RDSB" for example, finds HL's page about Shell. You owe it to yourself to save a packet on monthly fees. If you invest monthly at II the trades are free. And you still get one other free trade credit per month. No connection tyo II or AJ Bell other than a satisfied customer of both platforms.Originally posted by northernladuk View PostLeave a comment:

Leave a comment: